.png)

Lessons from the Icelandic vs Greek collapse

|

| Greek protesters clash with policemen during riots at a May Day rally in Athens May 1, 2010. Credit: Joanna CC-BY-SA 2.0 |

Debt = theft from future generations

All economic activity requires energy to perform useful work. Without an increasing flow of net energy to society the economy starts to contract. The extraction of finite fossil resources cannot sustain increased growth as depletion and diminishing returns eventually leads to bankruptcy and falling supply.

|

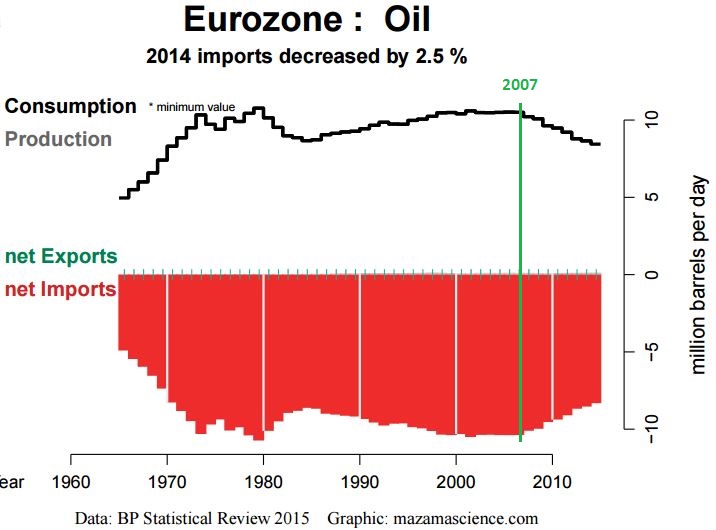

| Shows how the entire Eurozone has been contracting since 2007 as is visible in lower oil consumption. |

Monetization based on the assumption that the resource base is endless, which flies in the face of fundamental physics, can only lead to financial collapse. Intermediate stages that we have witnessed since 2008 is the erosion of the middle class, increased wealth inequality and increased numbers of poor people in society. Borrowing of work and resources from the future, through debt fuelled credit expansion, has become completely insane. To the extent that we are eroding the life-support systems that make up the basis for our own long-term survival. It has indebted future generations in ways they can never repay and is a grave intergenerational injustice.

Thermodynamic limitations of the physical world don’t even enter the grammar of most economists or central bankers who are wilfully inept to give advice on anything but how to ruin entire nations. The lack of a systems perspective has made the public unaware of the real dangers of a out of control financial system. Economic growth based on credit fuelled debt, which has exploded since the early 1980s, in form of unlimited issuance of government bonds, credit cards without security, sub-prime mortgages or quantitative easing are all just sophisticated ways of sending the bill to the future.

Its obvious that it's not possible to cure problems that arise from too much of something (debt) by doing more of it (piling on more debt). That's just insanity. If credit costs are larger than income minus other expenses then either the income must increase to balance losses or bankruptcy is the only way out. By now, we know that the pile of debt accumulated is unpayable and so a debt restructuring or debt jubilee is the only way forward. The young generation, especially, need to have their debts forgiven or we will have riots in the streets, political turmoil and an increase in crime rates.

|

| Protesters in front of the Alþingishús, seat of the Icelandic parliament, on 15 November 2008. Credit: Haukurth (CC BY-SA 3.0) |

Difference between purely financial and energy-induced collapse

In the fall of 2008 the financial system in Iceland collapsed leading to a closure of the three main banks and a 50% fall in the value of the Icelandic króna. When the banks collapsed they left huge obligations to lenders and customers without coverage. The Icelandic government issued a guarantee for all Icelandic accounts, releasing comparative demands from a large volume of overseas accounts (a net deficit of €3.2 billion after all assets were sold). The government had no way of covering this demand, causing the collapse of the Central Bank of Iceland and the currency. Iceland went bankrupt and loans in foreign currency became unpayable for state, businesses and private persons. The Icelandic people voted no in referendums to repay foreign debts, elected different people in office and jailed bankers for corruption. They basically had to restart the system. However, the real reason that Iceland has not suffered like Greece, for example, is because they were able to keep increasing their oil consumption (from imports) while relying heavily on domestic hydropower and geothermal for electricity production. This is not the case for the PIIGS countries which all were heavily reliant on oil imports that they could no longer afford.

|

| Data from the National Energy Agency in Iceland |

|

| Greece cannot afford to import more oil |

Many of the driving factors behind the Icelandic banking crisis and the GFC arose from a fundamental systems crisis in our present world. The economic model based on eternal financial and material growth has started to meet limits, where the human civilisation has outgrown the capacities of the planet to support it. Borrowing from the future to cover up this fundamental problem is a short sighted strategy that will come to an end, sooner rather than later. And it also means that the collapse curve will be even steeper as we have depleted more resources without making a transition to renewable energy resources.

Against such limitations, all talk or negotiations are futile, and pretending the dilemma does not exist has only lead to bigger risks with ever more debt - stealing from future generations. Countries may be able to handle a purely financial crisis, like Iceland, but they won't be able to handle a energy-induced financial crisis, like in the case of Greece. It doesn't matter what financial reforms they make as long as they can't afford the energy needed to operate society they will continue to contract. So while debt forgiveness is necessary it's not sufficient in solving Greece's problems.

{kind=link}

"Its obvious that it's not possible to cure problems that arise from too much of something (debt) by doing more of it (piling on more debt). That's just insanity"

ReplyDeleteYes, but..... for middle class families in mid-life, debt becomes the temporary solution for incomes being eroded by inflation, taxes, and fees imposed by a growing layer of government sanctioned middle-men.

The existing tax structure here is much more favorable to those willing to take on debt to finance a variety of assets, whereas personal austerity is severely punished by the tax man.

So the existing hierarchy actually rewards insanity, and punishes thrift and conservation. In a very real sense, we have to play the only hand that we're dealt.

As usual, I think your analysis is spot on. Just want you to see that the personal decisions we make are seldom black and white.

Yes, I agree that it's difficult for the individual and community to not take on more debt and that it's a structural problem. My criticism is largely on the policy level and of neoclassical economics which have dictated the rules the system now follows. To change incentives one has to change the basic rules of the game or nothing changes. The first step, however, is to recognize the fundamentals of the problem.

ReplyDelete