.png)

The big meltdown - 2020?

|

| Charles Blomfield's painting of the 1886 eruption of Mount Tarawera based on eyewitness accounts |

Contrary to the dominant narrative of “progress” I see major systemic crises converging towards the year 2020, or sooner! Are we reaching a major tipping point or simply another wave of entropy entering the system?

The symptoms of this can be found in the global economy itself with the rate of global growth stagnating (i.e. energy and debt limits) and tensions between countries competing for limited resources increasing. We also see it in the political sphere where maniacs with empathy deficit disorder get into power as a response to people's frustrations and start talking about all kinds of warfare: cultural, economic and military. We already see social unrest, conflict and trade wars but also talk about military wars connected to resources, mainly oil. Most societies are already very vulnerable, lack resilience to withstand further shocks, so a global financial meltdown could escalate fairly rapidly into chaos and destruction. When people lose everything, and they don't know why, they tend to get angry and violent. How will the US act? Will they unwind the empire, all military bases etc., or spend every bit of their last resources to plunder the planet? The place is more like an oligarchy so the über rich might decide they want the last of the oil, not for the people but for themselves. Europe is a basket case and is likely to break down, every nation on their own eventually. If a economic collapse doesn't do it, the flood of climate refugees will.

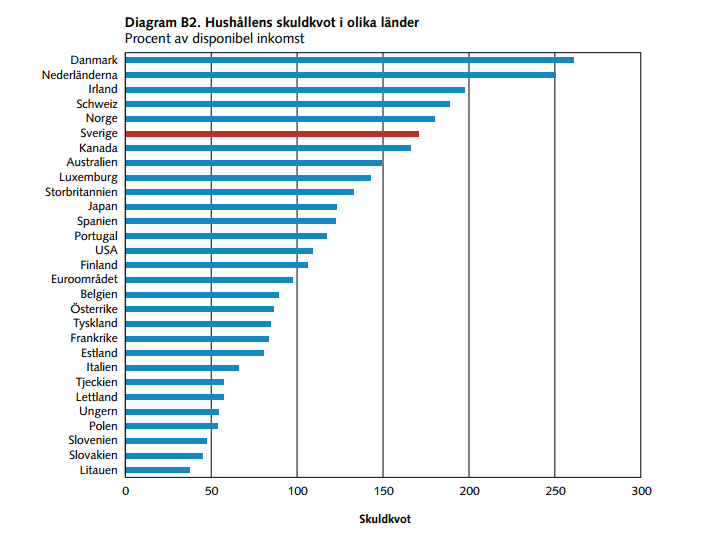

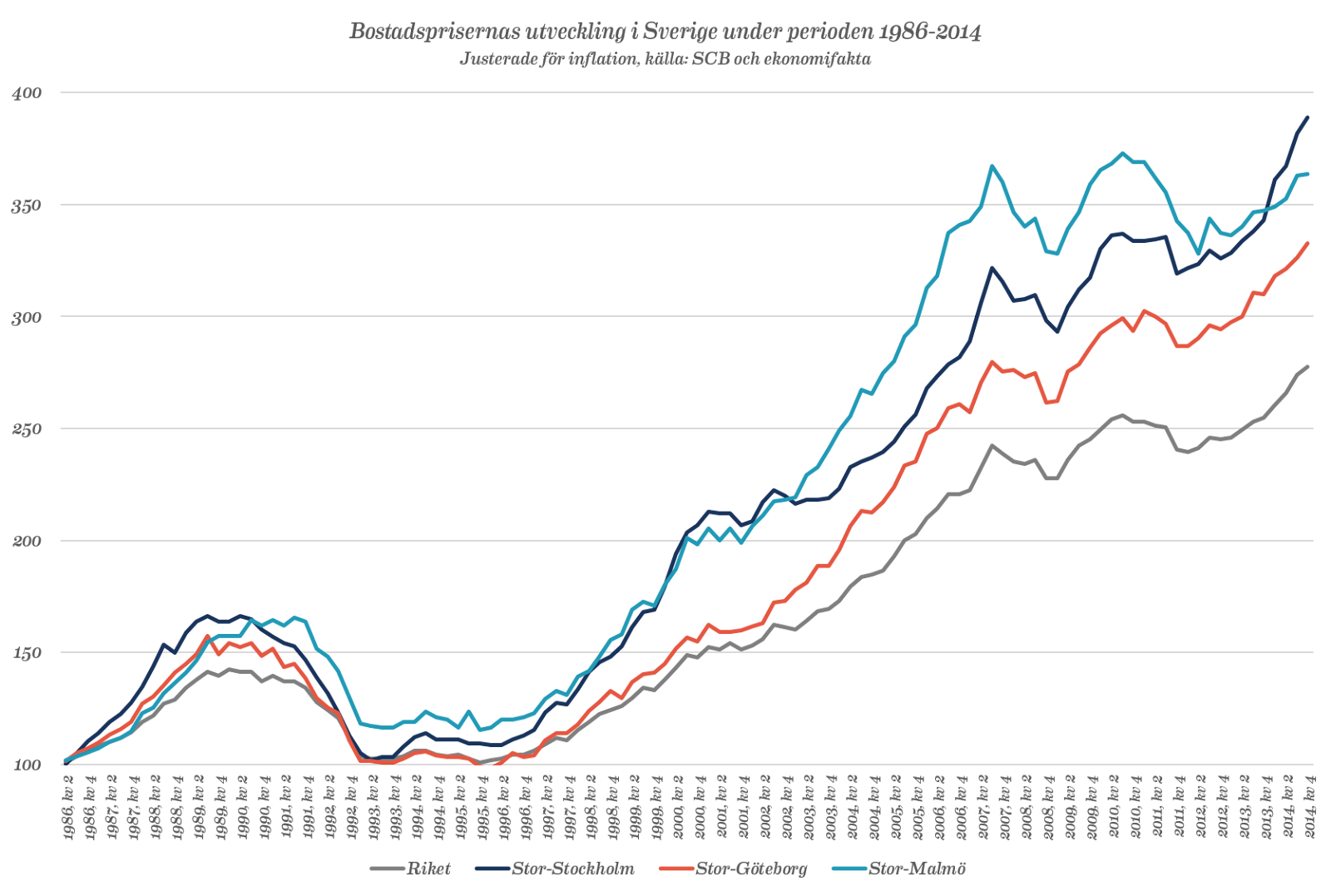

As for Sweden, we will see our massive housing bubble pop and a deep recession meanwhile people fleeing from the middle east will want to immigrate here. With the nationalist and xenophobic party, the Sweden Democrats, now being the third largest party things could turn out to their advantage as people become poorer and are likely to blame immigration issues. Similar to what we see in the rest of Europe. There is, however, a fairly strong left still in play in Sweden and to my surprise they got 10% of the votes in this year's election. So perhaps there is still some balance left in the political system, but without any major blocs the grownups in the government has yet to come to an agreement about how to rule, so maybe not. While they argue about who get what seat the world is on fire, and so it goes with large bureaucratic structures that become incompetent. And so the likelihood of social unrest increases.

As for the UN climate targets last chance of bending the emissions curve, I'm pretty pessimistic. A global financial meltdown will put all those hopes on hold and even if action did occur its likely too late to stop the climate from going above the 2C target. Moreover, what we need is not “green growth” but actual downsizing which would happen when the economy contracts. If we won't voluntarily give up consumption, mother nature will do it for us. But of course, it won't be what most people hoped for, it likely won't be a civilised and peaceful decent.

Will there be a global financial meltdown soon? Somewhere between 2018-2020? Well, I don’t know, but what's certain is that something has to give since we live on a finite planet where endless growth is impossible. There's no negotiating with nature.

{kind=link}

{kind=link}

{kind=link}

{kind=link}