Alternative energy technologies

Economic progress and wealth of society strongly depends on the best choice of energy supply techniques. Like with any living organism, societies needs energy to perform work. Before the industrial revolution we relied on horsepower, wood, wind and human labor. These forms of energy were, however, very inefficient because of their low energy density. It was not until we discovered coal and invented the stream engine that the revolution started and societal metabolism went up. Since then, humanity has been addicted to fossil fuels to propel our societies forward. Now, however, its becoming a real problem because the Earth is not as big as we thought. Fossil fuel extraction and pollution on a massive scale have caused our climate to change and we are running into limits of what the Earth can provide in terms of cheap and abundant natural resources. So we look to alternative technologies for solutions to this predicament. But as we know from the German case this issue is not without its challenges. We need a measurment that that can establish what alternative are most effective in terms of providing a net surplus of energy to society while reducing greenhouse gas emissions.

Energy return on energy invested

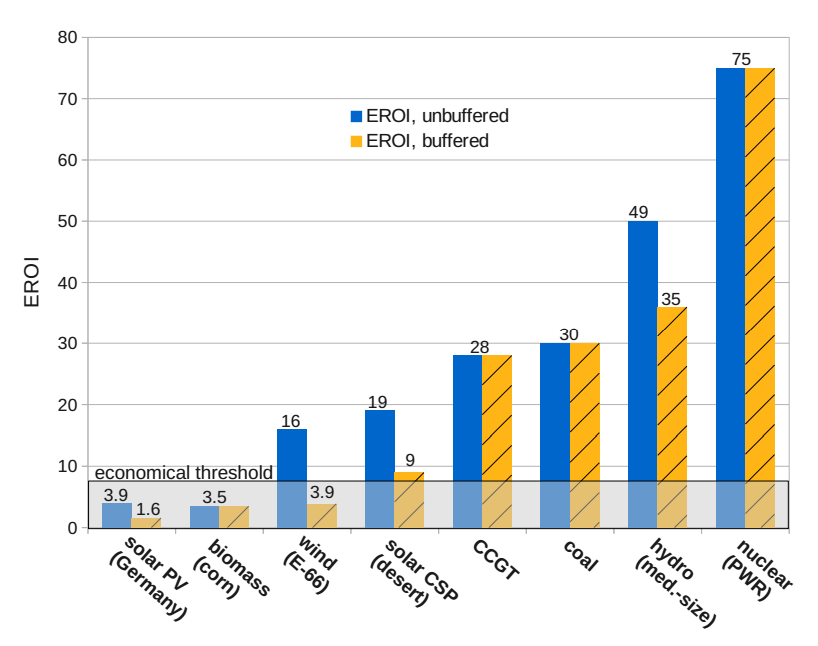

The energy return on (energy) investment (EROI) is an important measure that describes the overall life-cycle efficiency of energy supply techniques, independent of economical and political considerations. The EROI answers the simple question “how much useful (net) energy do we obtain for certain effort to make this energy available” (

Weißbach et al. 2013). As we know, energy and matter are never consumed or generated but always just converted. There is always a flow of materials (fuel, materials for construction, maintenance) driven by the “invested” energy with the result of making the “returned” energy available. This means that to calculate net energy of a particular supply technique, also known as carrier, one has to include all the energy it takes to produce electricity - from the extraction of resources to the construction and maintenance of the plant, as well as expected lifetime. Furthermore, because many so called renewable carriers are intermittent they usually require back-up plants or storage that can buffer for when they aren't generating enough electricity at times when people need it.

Weißbach et al. 2013 have chosen to include this in their EROI analysis, few others do. Break-even has an EROI of 1. But that would be pointless as you would have a plant but couldn’t run it. The higher the EROI the higher the return on investment.

As the graph above shows, solar photovoltaics and biogas from corn require so much energy that there is very little net energy provided to society, you put in 1 and get 3.9 or 3.5 back (even worse if you include the buffering). That’s not enough to run a complex society on. Wind onshore and hydropower, however, perform much better and give a return of 19 and 49 respectively. Natural gas and coal fired power plants give 28 and 30 in net energy. And nuclear has a value of 75, calculated with a 60 year lifetime. Solar thermal in the Sahara would also give enough net energy to be useful.

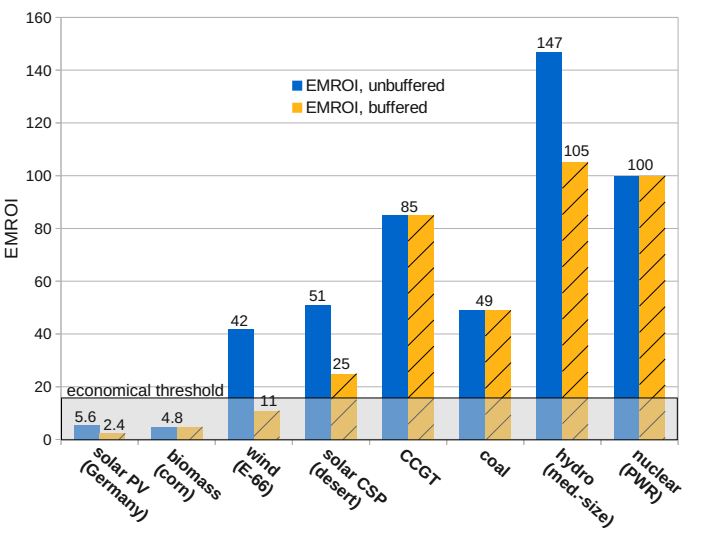

Energy Money Return on Investment

Now that we know which electricity producing technologies offer most in terms of net energy we can turn to monetary cost. But first note that not all energy is created equal. Electrical energy is very useful, because it can immediately do work. Heat and chemical energy are less useful because it's harder to get work out of them. By calculating the exergy, the available energy to do work, equivalent we can get energy money return on investment (EMROI). This is done by weighting both the energy inputs and energy output by a factor of 3 when the energy type is electrical. As shown in the graph below.

Because all these carriers produce electricity as output, but not all inputs are electric, the EMROI of all sources is higher than their EROI. This is one step further towards monetizing the EROI by allowing for the greater monetary value of electricity compared to other energy types. We can see that hydro, nuclear, natural gas and solar in the desert have high EMROI. However, EMROI is just a “best case” scenario for monetary return on investment. Note that the economic threshold has gone up to. The idea is that in e.g. the US, a kWh of energy cost about 10 cents but it produces about 70 cents worth of GDP, a ratio of 7 to 1. If we do the same computation in exergy terms, the ratio is 16 to 1. That means the fully monetary return on investment of exergy, for the economy as a whole, is 16. A similar ratio can be seen for other countries which leads to the conclusion that the thresholds are 7 for EROI and 16 for EMROI, assuming OECD-like energy consuming technology. For lower developed countries thresholds might be smaller, thus making also less efficient energies like biomass economic.

Greenhouse Gas Emissions

By looking at historical development rates of low-CO2 electricity production among different high-income countries we can try to figure out what techniques have worked well previously. Below is a chart showing OECD countries population size and generation of kWh per capita per year.

Overall we can see that only a few countries have succeeded to build low-CO2 electricity production with a rate of 300kWh/cap/year, which is the needed improvement speed to stay below the Kyoto Protocol 2 C degrees limit. One should note that no country have made it above the 300kWh/cap/year without the help of nuclear. We can see that Swedish nuclear development reached the highest level of 700 kWh/cap/year. Mean development rate only reached 120 kWh/cap/year between 1982 and 1992. When it comes to renewable electricity production, Denmark has the highest with about 160 kWh/cap/year. Closely followed by Sweden. Spain and Germany reached levels of 120 kWh/cap/year. We can see that Sweden has a top position in development rate of low-CO2 electricity production, both with nuclear and renewable energy. If the rest of the world would implement nuclear at the same rate as Sweden did, it would take 25 years to replace all existing fossil fuels (

Davour et al. 2014). It is very improbable that this will happen, and perhaps isn't recommendable, but the example show how important the inclusion of nuclear into the energy mix is for future low-CO2 electricity production.

Discussion

This is just one out of many studies that have looked at EROIs for various energy carriers. Because there is no universally accepted methodology one should be careful about taking any numbers for granted until reading the literature. These numbers are however in line with other studies, except in the case of nuclear. Previous studies have shown extremely varied numbers for nuclear. This could be because, since the 1980s when EROI measurements began, EROI for nuclear has been rising rapidly as the industry has switched from gas-diffusion enrichment of uranium to centrifuge (which is 35 times more energy efficient). The World Nuclear Association projects that there will be no more diffusion enrichment anywhere in the world by 2017. Moreover, there are other processes and a next generation of nuclear power plants, called Gen-IV designs, that don’t use enrichment at all which would give them much higher EROI. And Gen-IV models can't have a melt-down. The Chinese have 300 engineers working on a liquid-cooled thorium reactor right now. So if you wondered why

climate scientists like James Hansen are pro-nuclear, this is one reason.

Yes wind is fine if it can be grid-buffered against a non-fossil generating source and heavily subsidised. And yes we would need more hydro but many of the worlds rivers are already utilized and it can have massive effects on ecosystems and the hydrological cycle.

So if we want to eliminate fossil fuels from electricity production and if we want to manage that transition without wrecking the economy, nuclear may have to be part of the energy mix. I therefore think that we should support our

Swedish scientists in their wish to develop a Gen-IV lead-cooled test reactor that would reuse nuclear waste, minimizing the half life from 100 000 to 1000 years, sparing future generations the worries (

Davour et al. 2014). Unfortunately the Swedish government has not been able to make any clear decisions regarding our future energy system, and the future of nuclear research, despite the fact that many Swedes accept nuclear power and don't want to see eary decomission.

.png)

{kind=link}

{kind=link}