.png)

Oil and limits to debt expansion

Global Economic Slowdown

The global economy is slowing down and central bankers are getting nervous. Japan, Italy and Greece are all in recession. China is slowing down according to official statistics. Germany, France, Netherlands, and Sweden are all at stall speed (around 1% GDP growth). The US is doing better according to official statistics, showing nearly 4% growth for the two last quarters, but alternative statistics shows numbers closer to 2%. The Federal Reserve ended QE in October, now there are few forces left providing extra liquidity to the world’s markets. Oil and precious metal prices have fallen dramatically.

Deflation seems to be winning and could lead to major problems for the financial sector in 2015, similarly to what happened in 2008 when oil prices crashed to $45/barrel from hitting a price spike of $140/barrel, too high for the global economy to handle, fuelling a spiral of defaults and negative net credit creation that nearly caused the entire banking system in the developed world to collapse. Major price oscillations in oil could be the new normal as we encounter depletion of easy and cheap oil resources. The global economy cannot handle too high oil prices, but too low oil prices could also have big impacts, especially on exporting countries and financial energy markets.

Deflation seems to be winning and could lead to major problems for the financial sector in 2015, similarly to what happened in 2008 when oil prices crashed to $45/barrel from hitting a price spike of $140/barrel, too high for the global economy to handle, fuelling a spiral of defaults and negative net credit creation that nearly caused the entire banking system in the developed world to collapse. Major price oscillations in oil could be the new normal as we encounter depletion of easy and cheap oil resources. The global economy cannot handle too high oil prices, but too low oil prices could also have big impacts, especially on exporting countries and financial energy markets.

Oil price crash 2014

The price of Brent crude crashed to $61/barrel this week, its lowest since 2009. The speed of the drop, from $100/barrel in September, has caused many commentators to argue that central banks have lost the battle against deflation. Copper, oil, iron ore, coal, gold and silver are all showing signs of major economic weakness ahead.

The global economy needs oil for many purposes, for example to power transportation and produce food. If the oil price is too low, its not profitable to extract it. With low oil prices production may drop off rapidly. This can lead to a bunch of secondary effects. With low oil prices, it becomes increasingly difficult for expensive unconventional drilling operations (e.g. fracking, shale oil, tar sands) that are highly leveraged to pay back the loans they have taken out. Energy debt currently accounts for 16% of the US junk bond market, and the value of Venezuelan bonds recently fell substantially because of the high risk of default. Similarly, the Russian rouble has been in freefall which has driven up inflation, decreasing the Russian bank’s ability to pay off foreign debt.

The G20 plan

After the massive bank bailouts in 2008 there has been lots of discussions on how to change the system so new state bailouts won’t be needed. One proposal that has been discussed recently by the IMF and other institutions is to force bank depositors and pension funds to cover part of the losses, using Cyprus-style bail-ins. According to some reports, this approach has been approved by the G20 at their meeting in Brisbane (November 16, 2014). If this is correct, ordinary peoples bank accounts and pension plans could be at risk already. Sweden is not a part of G20 so we should not be affected by this.

Deflation winning?

Falling oil prices tend to lead to a lower price for producing food and other goods. The net result tends to be deflation. Not all countries are affected equally, some experience this to a greater extent than others. Those countries experiencing deflation are likely to eventually get problems with debt defaults because. Investers could flee the country since they can’t make an adequate return and this usually tend to push currencies down, relative to other currencies. In Russia this is the case right now. Since the dollar has been rising rapidly, debt repayment is likely to be of greatest concern to those countries where substantial debt is denominated in US dollars but whose local currency has fallen in value. Countries with low currency prices such as Japan, parts of Europe, Brazil, Argentina and South Africa could find it expensive to import goods of all kinds. The Chinese yuan is closely tied to the dollar which makes Chinese exports more expensive and may be part of the reason why their economy has slowed down recently. However, China also have massive debts and a shadow banking system that could be huge. No one really knows since the Chinese aren't transparent with their accounting.

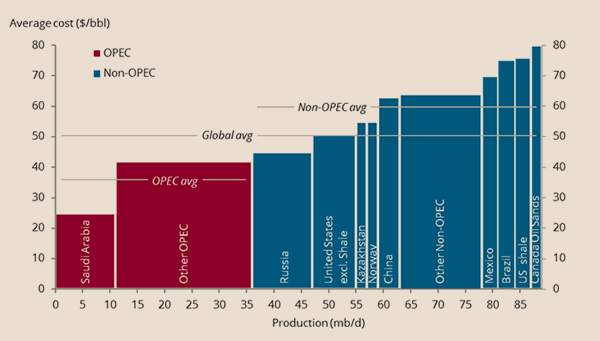

|

| Oil production break even prices. Source: Energy tracker via FT |

Limits to debt expansion

There are limits to the amount of debt that a government, or business can borrow. At some point, interest payments become so high that its difficult to cover other expenses. The way around this have been to lower interest rates to zero. The problem is that we have a monetary system that is either expanding or collapsing. It has no steady state. Increasing debt has been a big part in pumping up demand for commodities and ensuring some economic growth. But interest rates can only go so low and QE does not work in the long-term, mostly it just creates asset bubbles and risky investments. The oil price fall started almost at the same time as the FED ended QE3 in October this year (the crash in oil prices in 2008 was credit-related and prices only picked up after the US initiated its program of QE in November 2008).

Zero interest rates and QE allows more borrowing from the future than would be possible if market interest rates really had to be paid. This allows financiers to temporarily disguise a growing problem of unaffordability of oil and other commodities. The problem is that we live in a finite world and we have reached a point where it has become more expensive to produce essential commodities. Wages don’t rise correspondingly, in most countries, because more and more labor is needed to provide less and less actual benefit. Workers find themselves becoming poorer in terms of what they can afford to buy. So even if prices for basic goods drop, fewer jobs and lower wages keep consumers from spending. Once commodity prices fall to levels that are affordable based on the income of consumers, they fall to levels that cut out a large share of production.

The timing of defaults and debt-related problems can take time. Low oil prices take a while to work their way through society. It is also possible that central bankers decide to take up another round of QE early in 2015, or that oil prices hit a low and start going back up. Limits to cheap energy could play out through lower oil prices as limits to growth in debt are reached and demand is destroyed. A collapse in oil production as a consequence of low oil prices could be much more severe for the global economy.

0 kommentarer: